A Competency Framework for BFSI is a systematic model that establish the knowledge, skills, behaviors, regulatory awareness, customer-centric capabilities, risk management competencies, and leadership attributes which are required in banking, financial services, and insurance organizations. Unlike generic competency frameworks, BFSI-specific models bring in compliance, governance, digital banking, financial risk, cybersecurity, and customer trust factors that really influence business performance, regulatory adherence, and organizational sustainability.

Key Takeaways at a Glance

|

Area |

Generic Competency Models |

BFSI-Specific Competency Framework |

|

Compliance |

Secondary consideration |

Core business capability |

|

Risk Management |

Generic awareness |

Strategic competency |

|

Customer Trust |

Soft skill |

Business-critical asset |

|

Digital Banking |

Optional |

Essential capability |

|

AI Readiness |

Rarely included |

Future necessity |

|

Cybersecurity |

Technical function only |

Enterprise-wide responsibility |

|

Leadership |

Management focused |

Ambiguity-focused leadership |

|

Talent Development |

Role-based |

Future-readiness based |

Why Does BFSI Need a Specialized Competency Framework?

Banks, NBFCs, insurance companies, and fintech institutions operate on one of the most regulated and risk-sensitive industries. A generic competency framework often miss out the importance capabilities such as compliance management, fraud prevention, credit underwriting, risk assessment, and customer trust-building. A diligent Competency Framework for BFSI integrates workforce capabilities with business goals, regulatory expectations, and industry transformation.

For decades, competency frameworks focuses on performance management, learning interventions, and succession planning. While these remain important, they are not longer able to manage the certainties which are faced by banks and NBFCs.

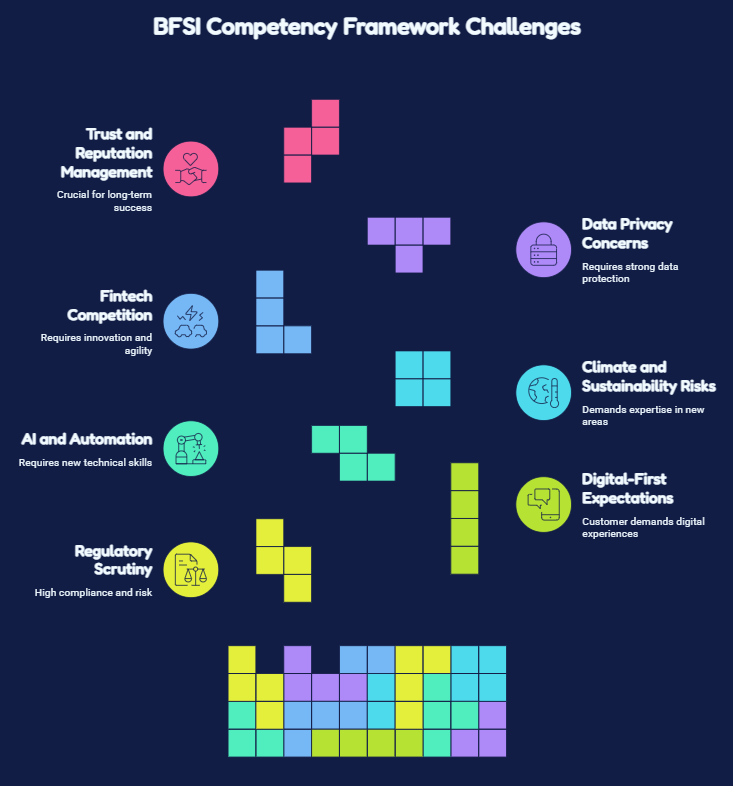

Today’s financial institutions operate on:

- Artificial Intelligence and automation

- Regulatory scrutiny

- Digital-first customer expectations

- Climate and sustainability risks

- Fintech competition

- Data privacy concerns

- Trust and reputation management

These challenges demand more than technical expertise.

For example, a relationship manager at a manufacturing company and a relationship manager at a bank may share communication skills. However, banking professionals must needs to additionally be aware about the KYC norms, AML regulations, credit assessment principles, customer due diligence, financial products, and regulatory compliance.

This is where a robust Competency Framework for BFSI is needed.

Source: Clearingpost

Did You Know?

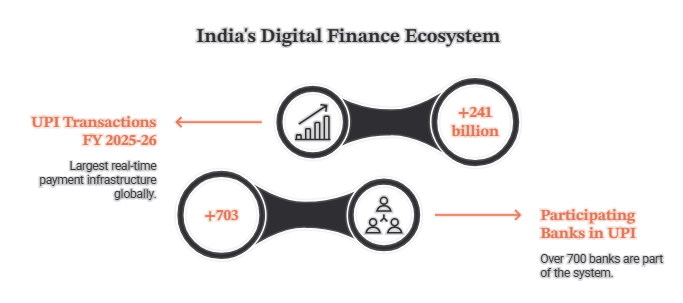

India’s digital finance ecosystem is now moving at an unprecedented scale. UPI handled more than 241 billion transactions in FY 2025-26, with over 703 participating banks, and honestly, it feels like one of the world’s largest real-time payment infrastructures.

What Makes a Competency Framework for BFSI Different from Generic Models?

A Competency Framework for BFSI varybecause it combines regulatory compliance, financial risk management, customer trust, governance standards, digital capabilities, and industry-specific technical expertise. Generic frameworks normally focuses only on leadership, communication, teamwork, and problem-solving skills.

In our experience adopting these frameworks for financial firms, generic competency models create 3 significant gaps:

1. Compliance Blind Spots

Financial institutions operate under strict regulatory supervision. Employees need to understand:

- RBI regulations

- AML guidelines

- KYC requirements

- Data privacy standards

- Fraud prevention controls

A traditional competency framework hardly evaluates these capabilities.

2. Risk Management Deficiency

Risk is the baseline where banking operations are being performed.

Whether managing:

- Credit risk

- Market risk

- Operational risk

- Cybersecurity risk

- Reputation risk

Employees need specialized competencies that generic frameworks fail to measure.

3. Customer Trust and Ethical Judgment

Trust delivery, customer retention and regulatory confidence.

The best Competency Framework for BFSI includes:

- Ethical decision-making

- Financial advisory capability

- Customer transparency

- Responsible lending practices

- Fair treatment principles

These are particularly important when executing the guidelines on fair practices code for NBFCS and customer protection frameworks.

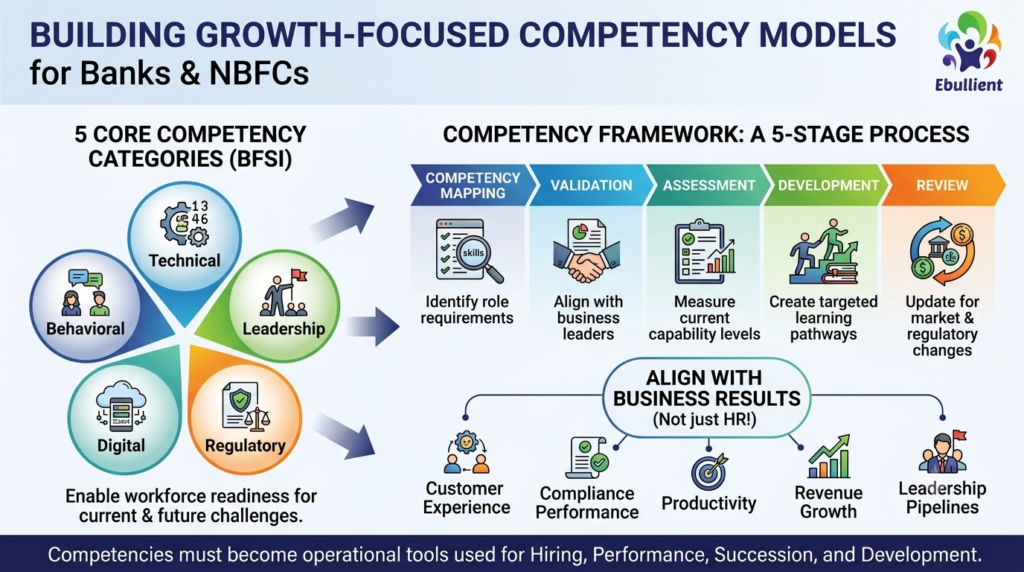

Which Core Competencies Should Every BFSI Organization Include?

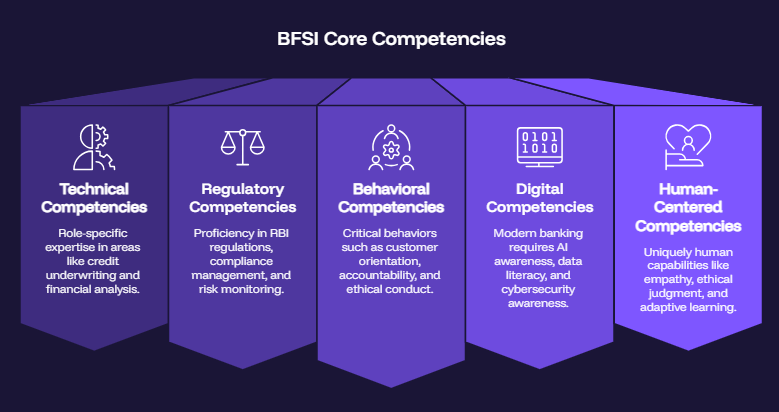

Every Competency Framework for BFSI needs to have 5 categories: technical competencies, behavioral competencies, leadership competencies, digital competencies, and regulatory competencies too. All of these make sure that workforce readiness for current as well as future business challenges.

Technical Competencies

Role-specific expertise, such as that which includes:

- Credit underwriting

- Treasury operations

- Financial analysis

- Lending operations

- Investment advisory

- Insurance underwriting

Regulatory Competencies

Employees should prove proficiency in:

- RBI regulations

- Compliance management

- Internal controls

- Governance standards

- Risk monitoring

Organisations should align these capabilities with the latest best rbi guidelines for NBFC requirements and operational standards.

Behavioral Competencies

Critical behaviors include:

- Customer orientation

- Accountability

- Collaboration

- Ethical conduct

- Decision-making

Digital Competencies

Modern banking requires:

- AI awareness

- Digital transformation understanding

- Data literacy

- Automation adoption

- Cybersecurity awareness

Human-Centered Competencies

As technology keeps expanding, their uniquely human capabilities which are becoming more valuable:

- Empathy

- Ethical

- judgment

- Collaboration

- Trust-building

- Adaptive learning

These competencies help organisations shift from seeing people as resources too, to realizing them as real human beings that have creativity, care, and wisdom.

How Can Banks and NBFCs Build Competency Models That Support Business Growth?

Every Competency Framework for BFSI must have have 5 categories, technical competencies , behavioral competencies, leadership competencies, digital competencies and regulatory competencies. All of these enable workforce readiness for current as well as future business challenges.

Banks and NBFCs must design competency frameworks around business results rather than HR processes. The most successful models connect competencies directly improves customer experience, compliance performance, productivity, revenue growth, and leadership pipelines.

Many organisations are searching for bank and NBFC models when beginning this process.

A successful framework generally follows five stages:

| Stage | Purpose |

|---|---|

| Competency Mapping | Identify role-specific requirements |

| Validation | Align with business leaders |

| Assessment | Measure current capability levels |

| Development | Create targeted learning pathways |

| Review | Update for market and regulatory changes |

Real Example: Kotak Mahindra Bank

Kotak Mahindra Bank has continuously invested in leadership development and capability-building programs to boost customer service, digital transformation, and risk management functions. Competencies should not remain with the HR department. They must become operational tools used for hiring, performance management, succession planning, and leadership development.

Real Example: Bank of India

Bank of India (BOI) continues to prioritize employee capability development by leveraging training initiatives focused on digital banking, compliance, customer service, and operational excellence.

This shows how public-sector institutions gets benefit from systematic competency frameworks drives business priorities.

Source: Ibef

Did You Know?

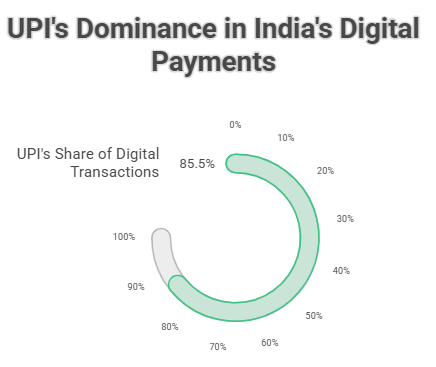

Based on RBI-linked industry reports , UPI was responsible for roughly 85.5% of India’s total digital payment transaction volume through the second half of 2025.

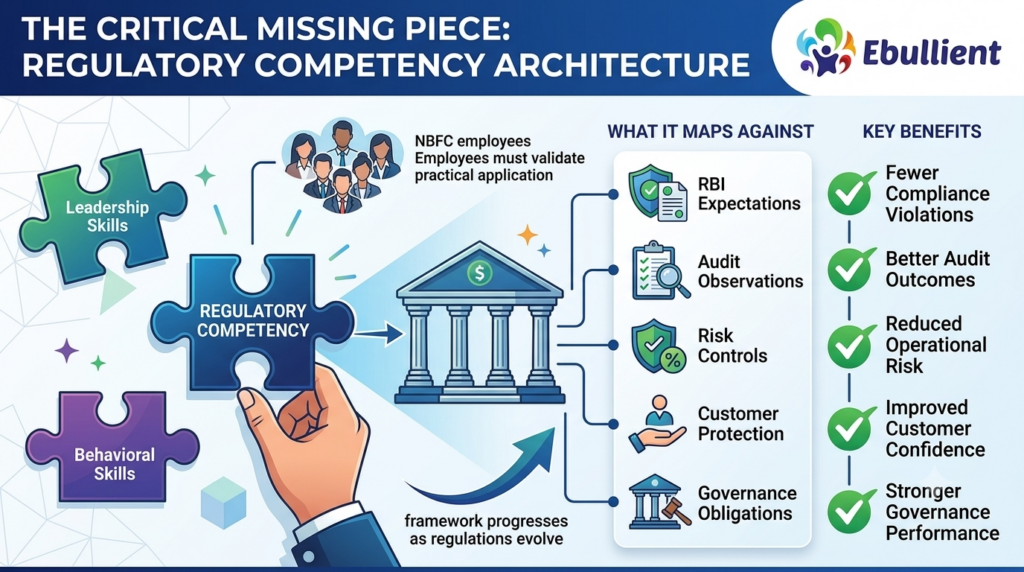

The Critical Missing Piece: Regulatory Competency Architecture

Many organisations needs to build competency frameworks around leadership and behavioral skills but neglecting regulatory competency architecture.

This is one of the most costly mistakes in BFSI.

A regulatory competency architecture maps competencies against:

- RBI expectations

- Audit observations

- Risk controls

- Customer protection requirements

- Governance obligations

For NBFCs, understanding the rbi guidelines for nbfc pdf documentation is only the initial phase to starts from. Employees must validate practical application of regulatory requirements in daily decision-making.

As regulations evolve, competency frameworks should also progress.

Organisations that regularly update their Competency Framework for BFSI often experience:

- Fewer compliance violations

- Better audit outcomes

- Reduced operational risk

- Improved customer confidence

- Stronger governance performance

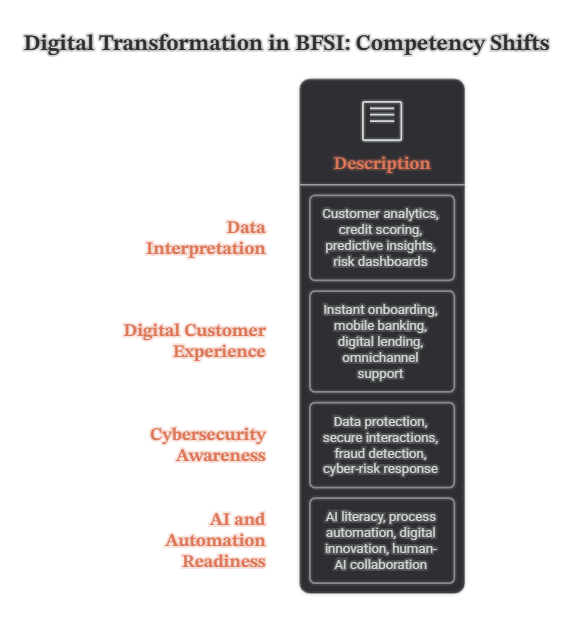

How Is Digital Transformation Reshaping Competencies in BFSI?

Digital transformation, its fundamentals are rapidly shifting workforce requirements across banks, insurance firms , and NBFCs. Employees need to blend both the usual financial expertise links, and also some digital fluency, with technology adoption, data-centric decision-making, and a more hands-on approach.

Also, the rise of fintech NBFC companies in India has really accelerated the competition.

Today’s workforce requires competencies in:

Data Interpretation

Employees increasingly work with:

- Customer analytics

- Credit scoring models

- Predictive insights

- Risk dashboards

Digital Customer Experience

Customers expect:

- Instant onboarding

- Mobile banking

- Digital lending

- Omnichannel support

Employees require these systems to deliver seamless and smooth service.

Cybersecurity Awareness

Cyber threats continue to grow across financial institutions.

Competencies should include:

- Data protection awareness

- Secure customer interactions

- Fraud detection

- Cyber-risk response

AI and Automation Readiness

Future competency frameworks increasingly to a greater extent:

- AI literacy

- Process automation understanding

- Digital innovation capability

- Human-AI collaboration

This is important as banks and NBFCS models in india evolve toward digital-first operating structures.

Source: Worldline

Did You Know?

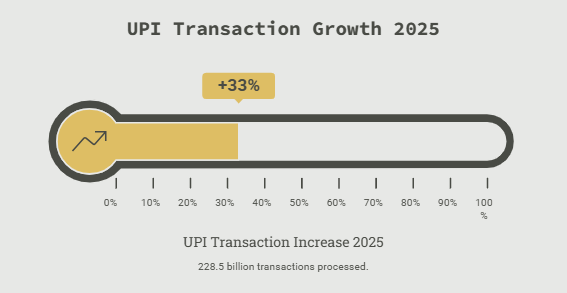

In 2025 UPI processed about 228.5 billion transactions, and that’s roughly a 33% year-on-year increase.

How Can a Competency Framework Support Growth and Succession Planning?

A strategic Competency Framework for BFSI enables organisations to identify future leaders by closing capability gaps, improving the hiring process, boosting employee development, and developing resilient succession pipelines.

The rapid NBFC growth in India is creating ongoing demand for capable leaders.

Many organisations are still struggling to answer:

- Who is ready for leadership?

- Which capabilities are missing?

- How should future leaders be developed

Competency frameworks offer these answers.

Leading organisations use competency data to:

- Enhancing recruitment decisions

- Guide learning investments

- Identify high-potential employees

- Build leadership pipelines

- Support organisational transformation

Even firms reviewing an expanding nbfc company list for benchmarking increasingly recognize that capability—regulate long-term success.

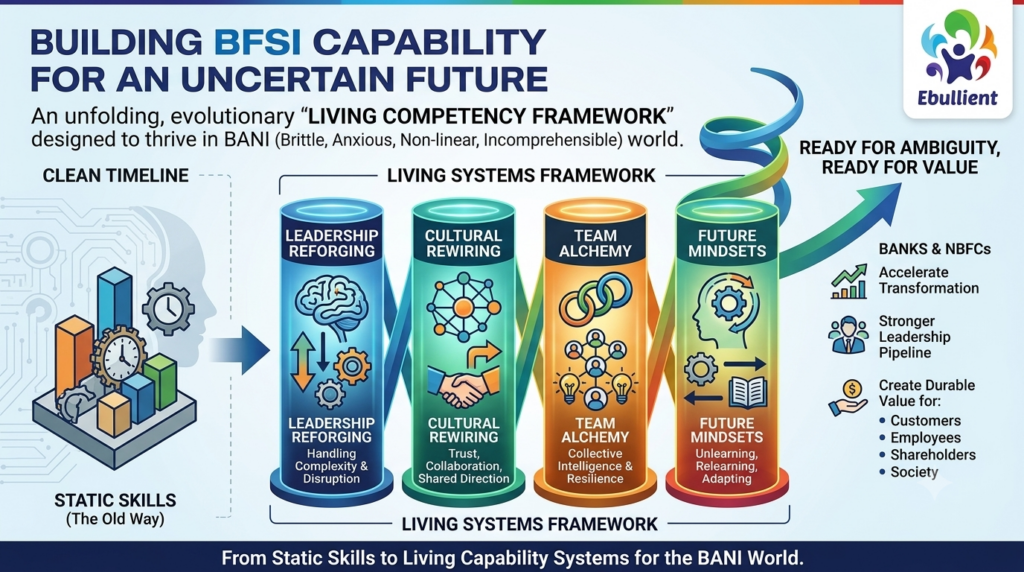

How Ebullient Helps BFSI Organizations Build Capability for an Uncertain Future?

At Ebullient Consultancy, we helps in developing competency frameworks , but it must do more than just redefining skills— it also needs be prepare organisations to thrive amidst disruption.

We focus on :

Leadership Reforging

Building mindsets that can handle complexity, uncertainty, and disruption.

Cultural Rewiring

Creating ecosystems of trust, collaboration, and a shared sense of direction.

Team Alchemy

Encouraging relationships, real resilience, and collective intelligence.

Future Mindsets

Helping leaders keep unlearning, relearning, and adapting as the ground moves.

In a BANI world, marked by uncertainty and rapid movement, competency frameworks can’t stay static; they need to become living systems that keep changing with the business reality.

Banks and NBFCs that take this shift seriously will be more ready for ambiguity, able to transform, build stronger leadership pipelines, and create durable value for customers, employees, shareholders, and society.

Frequently Asked Questions

Get answers to commonly asked questions about Ebullient.

Why do generic competency frameworks fail in banking and NBFC environments?

What is a Competency Framework for BFSI?

Competency Framework for BFSI is basically a systemic model that lays out the knowledge, skills, behaviors, the technical know-how, and even the regulatory readiness that you’d need to actually succeed inside banking, financial services and insurance firms.

Why can’t banks use generic competency frameworks?

Generic frameworks often overlook compliance, risk management, financial expertise, governance, and customer trust competencies that are critical for BFSI operations.

How often should a BFSI competency framework be updated?

Most organizations should do a review annually, and then make bigger revisions every two to three years. This helps them stay them relevant with new regulatory expectations and shifts in business priorities.

What competencies are most important for NBFC employees?

Generally, the most important ones are regulatory compliance, credit assessment, customer service, ethical conduct, risk management, digital literacy, and also business development readiness.

How does competency mapping support succession planning?

Competency mapping supports future leadership potential, it flags capability gaps early, and it supports building structured succession pathways for those critical roles.