Digital banking trends in 2026 will be defined by AI-driven personalisation, integrated financial systems, real-time payment solutions, blockchain technology deployment, and banking services that operate through platform ecosystems. The financial institutions transform their operations through these innovations which improve customer experiences, boost operational efficiency, and drive revenue optimisation to create agile data-driven systems that focus on customer needs in order to compete with rapid changes in the digital-first economy.

Key Takeaways – At a Glance

-

Digital banking trends have redefined customer experience and business models.

-

The tools like AI and data analytics are controlled by the needs of personalisation together with the demands of operational efficiency.

-

Embedded finance and BaaS create new opportunities for businesses to generate revenue. Security requirements together with compliance needs stand as the most important business priorities.

-

The process of organisational transformation needs training programmes together with upskilling initiatives.

-

The future digital banking trends will be an integrated system which uses intelligent technology to provide services that focus on customer needs.

What Are Digital Banking Trends and Why Do They Matter in 2026?

The term ‘digital banking trends’ refers to the technological and strategic changes which are currently reshaping financial service delivery through the implementation of AI and blockchain and open banking and embedded finance systems which aim to improve customer service and operational performance.

Digital banking has completely transformed the ways in which customers and businesses interact with money. The banking experience has evolved from online account access to a complete system which enables users to manage their payments and loans and investments and financial planning activities.

The digital banking system brings a complete transformation of banking operations because it establishes banking services as permanent elements within users’ daily tasks through their mobile applications and web platforms and digital ecosystems.

The rapid adoption from India to global markets has enabled customers to experience seamless 24/7 access while banks reduce operational costs and leverage data-driven insights. This evolution defines the future of digital banking.

Source: Back Base

Did You Know?

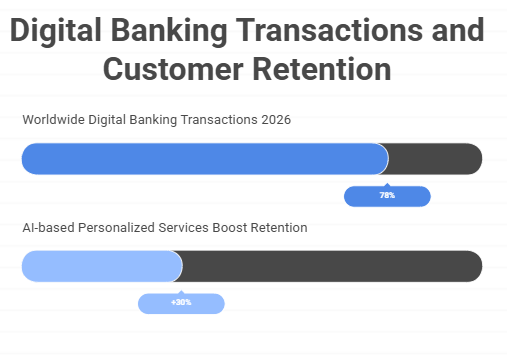

More than 78% of worldwide banking transactions will take place through digital channels by the year 2026, according to predictions that state that AI-based personalized services will boost customer retention rates by almost 30%.

What Does Digital Banking Mean in 2026?

Digital banking in 2026 extends beyond apps and portals to include artificial intelligence and blockchain technology and cloud computing and embedded finance to develop a complete financial system.

The present digital banking system combines modern technological solutions with current customer patterns and compliance requirements.

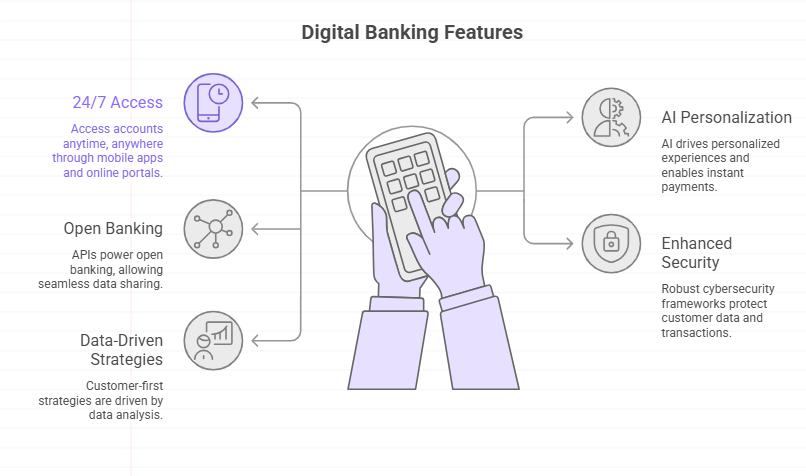

The 2026 Digital Banking system’s main features are the following:

- 24/7 account access via mobile apps and online portals.

- AI-driven personalization and instant payments.

- Open banking powered by APIs.

- Enhanced cybersecurity frameworks.

- Data-driven customer-first strategies.

The banking industry currently observes three major trends that will boost global digital banking net interest income according to market forecasts.

What Are the Top Digital Banking Trends in 2026?

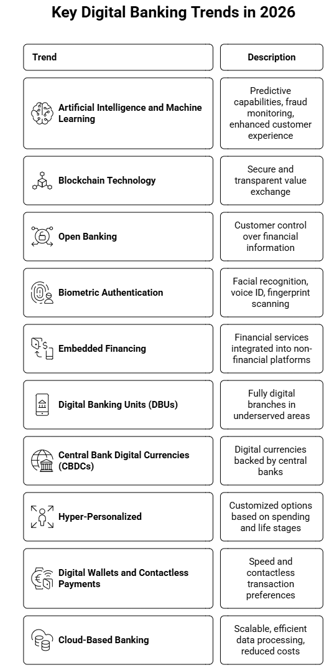

The top trends for banking in 2026, the era of unconstrained banking, include AI, blockchain, open banking, embedded finance, digital wallets, cloud banking, CBDCs, and hyper-personalisation.

1. Artificial Intelligence and Machine Learning

Financial institutions are using AI and machine learning to provide predictive capabilities, monitor for fraud in real time, and enhance the customer experience. AI and machine learning enhance efficiency, eliminate many manual processes, and create hyper-personalized products that integrate into individual spending patterns and life changes

2. Blockchain Technology

The rise of blockchain will create new ways to securely and transparently exchange value. Usage includes smart contracts, enhancing cross-border payments, and expanding KYC processes. This modern technology is creating trust and reducing fraud, particularly in populations that have adopted technology

3. Open Banking

Open banking is about the power of the customer over their financial information. Calling on customer permission, third-party providers can access data through open APIs that will create more competition, innovation, and tailored products. The openness of banking has evolved further in the UK and EU with the implementation of PSD2 regulation (and will quickly be making its way to other regions)

4. Biometric Authentication

Facial recognition, voice ID, and fingerprint scanning are quickly becoming mainstream. Not only do biometrics enhance security levels, but they streamline login processes and reduce the onus on customer-created passwords.

5.Embedded Financing

Financial services are being more and more incorporated into non-financial platforms. Retailers, travel companies, and even health care providers incorporate payment, insurance, and lending into their apps. For example, Indian applications, like Ola, already embed loans, insurance, and wallet services in relation to their transport offerings.

6.Digital Banking Units (DBUs)

Digital Banking Units are changing the landscape of financial inclusion by acting as fully digital branches in underserved areas. DBUs could offer paperless account opening, remote support, and digital lending capability, providing the opportunity for rural and semi-urban populations to access formal banking sources at a lower cost.

7.Central Bank Digital Currencies (CBDCs)

Over the past year, more than 100 central banks have either tested or are poised to launch digital currencies. India’s e-Rupee and China’s Digital Yuan are leading the way in establishing parameters for how digital currency which could be backed by a central bank could change payments, auditing, and cross-border trade

8.Hyper-Personalized

Data analytics and AI have emerged whereby banks can be the “Netflix of finance” as banks can now upload customized options for products, loans, or investment plans based on spending patterns, financial objectives, and life stages.

9. Digital Wallets and Contactless Payments

The rise of wallets like Amazon Pay, HDFC Pay, and ICICI Pay points to the speed and contactless transaction preferences of millennial and Gen Z consumers, and these will surely accelerate as the digital-first generations increase

10. Cloud-Based Banking

. Using the cloud provides local banks the ability to scale more rapidly, more efficiently aggregate and process large quantities of data, and reduce infrastructure costs. Cloud-enabled banking platforms also facilitate greater service innovation and speed to market.

Source: Ozone Api

Did You Know?

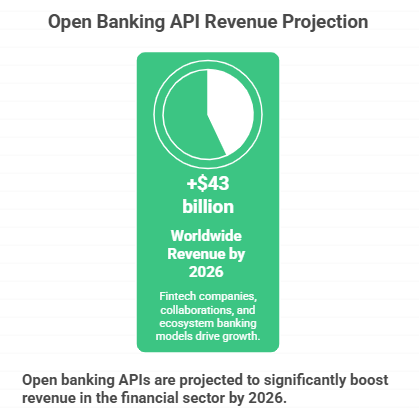

The financial sector expects open banking APIs to generate more than $43 billion in worldwide revenue by 2026 because fintech companies and collaborations and ecosystem banking models.

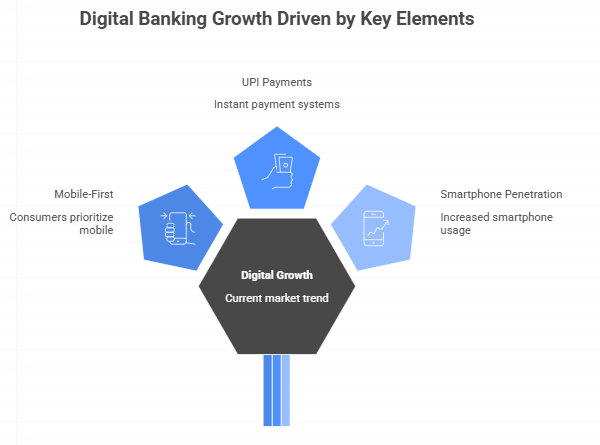

How Are Digital Payments Driving Banking Transformation?

The digital payment system is driving a banking revolution through its ability to deliver quicker cashless payments and its capacity to enhance financial access for customers.

The worldwide digital transaction volume will reach over USD 8.5 trillion, which demonstrates that societies are quickly moving away from cash usage.

The current growth pattern has its support from three main elements, which include the following:

- Mobile-first consumers

- UPI and instant payment systems

- Increased smartphone penetration

The current market trend forces banks to allocate funds toward building their basic infrastructure so that it can support upcoming digital banking technologies.

Why Is Security Still the Foundation of Digital Banking?

Digital banking needs security measures because they help safeguard customer information and stop fraudulent activities and protect people who use financial systems.

Cybersecurity threats increase with the rise of digital adoption. Banks are investing heavily in:

- AI-driven fraud detection

- Encryption technologies

- Multi-factor and biometric authentication

Our experience with security framework implementation in financial institutions demonstrates that trust functions as the main factor which builds customer loyalty to digital banking services over the years.

What Are the Different Types of Digital Banking Models?

The two major types of digital banking include neobanking, challenger banking, digital-only banking, and traditional banking with digital capabilities.

| Type | Description | Strategic Value |

|---|---|---|

| Neobanks | Fully digital banks | Cost efficiency |

| Challenger Banks | Compete with traditional banks | Innovation |

| Digital Extensions | Legacy banks going digital | Customer retention |

| BaaS Platforms | Banking infrastructure providers | Ecosystem expansion |

How Are Digital Banking Units (DBUs) Driving Financial Inclusion?

DBUs provide complete digital banking services to underserved regions, which let customers access financial services without needing physical bank locations.

DBUs provide their most beneficial services to developing economies, which include India, as their target market. The services include

- Paperless account opening

- Remote support

- Digital lending services

The process reduces operating expenses while it increases access to banking services, which exist as a fundamental element of digital banking trends.

Source: McKinsey

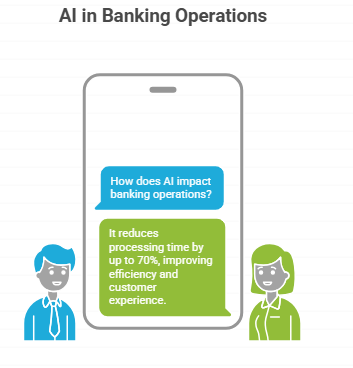

Did You Know?

Banking operations that use artificial intelligence technology achieve processing time reductions of up to 70%, which results in enhanced operational efficiency and better customer experiences.

A Critical Shift: Banking at the Intersection of Technology, Purpose, and Humanity

The next phase of digital banking will enable financial institutions to develop technological solutions which will improve their operational efficiency while maintaining their core ethical principles.

The core of Ebullient’s philosophy exists at this particular moment.

The current banking system functions through three fundamental banking elements, which are:

- The digital revolution

- The sustainability imperative

- The purpose movement

Financial institutions need to develop beyond their current systems and processes because they operate in a world where technological progress develops at an accelerated pace. Financial institutions need to develop essential abilities through which decision-makers will use their system capacities to operate when faced with uncertainty.

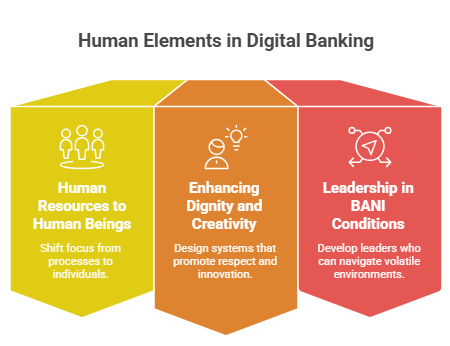

This transition means:

- Moving from “Human Resources” to “Human Beings”

- Designing systems that enhance dignity, creativity, and care

- Building leadership that thrives in BANI conditions

The transformation of digital banking requires both technological advancements and fundamental changes in human behaviour.

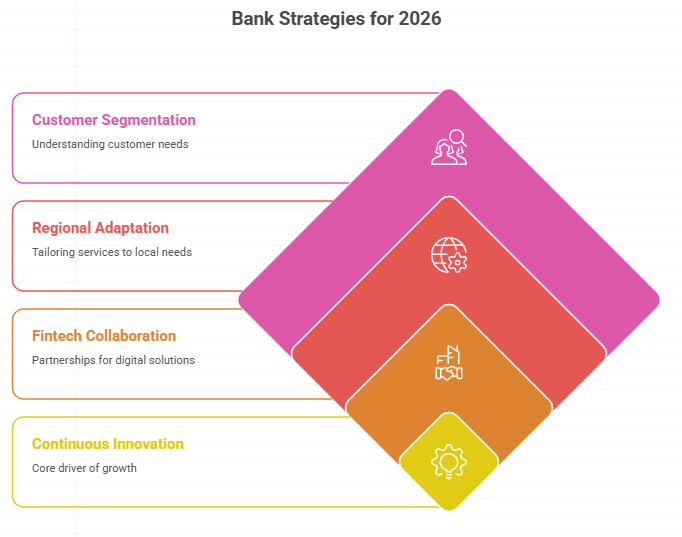

What Strategies Should Banks Adopt in 2026?

Banks must focus on four areas, which include customer segmentation and regional adaptation and fintech collaboration and continuous innovation to maintain their market position.

Key Strategies:

- The customer segmentation should be conducted through the analysis of demographic information and behavioural patterns.

- The organisation needs to develop tailored solutions which address the specific requirements of different regional markets.

- The organisation needs to establish partnerships with fintech ecosystems.

- The organisation needs to allocate resources to develop its capacity for making decisions based on data analysis.

The banks which implement digital banking trends through strategic alignment achieve higher performance compared to their industry rivals, according to our consulting experience.

How Ebullient Supports Digital Banking Transformation?

Ebullient helps organisations adopt digital banking technologies through targeted corporate training, which prepares employees to execute business strategies.

Here’s the reality for L&D leaders: technology adoption will not succeed without proper skill development programmes.

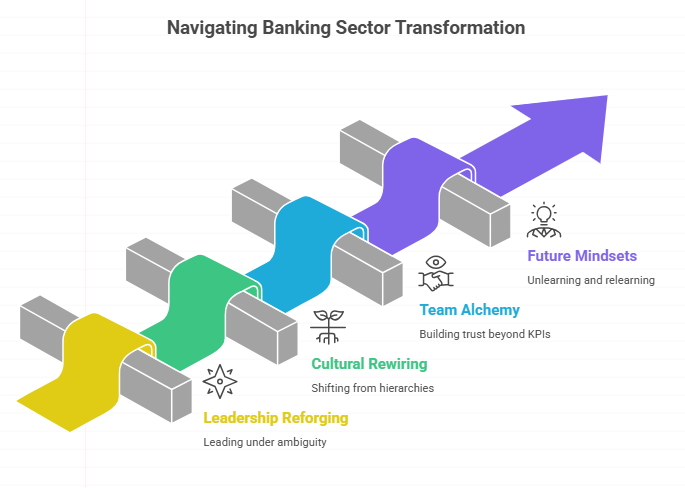

Ebullient addresses this by focusing on:

1. Leadership Reforging

Developing mindsets, not just technical skills, to lead under ambiguity.

2. Cultural Rewiring

Shifting from rigid hierarchies to adaptive ecosystems.

3. Team Alchemy

Building trust-driven, high-performing teams beyond KPIs.

4. Future Mindsets

Encouraging unlearning and relearning to stay relevant.

Their programs, including best digital banking trends training and banking as a service training, equip organizations to align with recent trends in banking sector while staying human-centered.

What Does the Future of Digital Banking Look Like Beyond 2026?

The future of digital banking will operate through autonomous systems which use embedded technology to deliver intelligent services that focus on human needs.

The future of banking will develop through three main financial service elements, which include

- The first element establishes invisible financial services.

- The second element uses artificial intelligence to control all financial decision-making processes.

- The third element enables customers to connect their financial services with all other aspects of their life through complete system integration.

The top banking trends for 2026 create a vision which shows the development of unrestricted banking operations.

The top trends for banking in 2026, the era of unconstrained banking, but their business success depends on how they make technology understandable for people.

Final Thoughts

Digital banking trends revolutionise banking operations while establishing new financial systems throughout the entire financial ecosystem. Technology investments without corresponding people development will create difficulties for organisations that want to achieve success.

The successful approach integrates three elements, which are innovative methods and flexible operations and development of organisational competencies. For decision-makers, the question is no longer “Should we transform?” but “How fast can we adapt?”

Ebullient believes the future belongs to organizations that humanize technology—creating financial ecosystems that are not only efficient but also inclusive, ethical, and sustainable.

Frequently Asked Questions

Get answers to commonly asked questions about Ebullient.

What are the top digital banking trends shaping the financial sector in 2026?

What are the most important digital banking trends in 2026?

The digital banking trends experiences the most impactful disruption from AI, blockchain technology, embedded finance systems, open banking frameworks, and real-time payment methods.

How is AI used in digital banking?

AI enables digital banking operations through three main functions, which include fraud detection systems and predictive analytics capabilities and creation of customised services for users.

What is Banking-as-a-Service (BaaS)?

BaaS enables businesses to deliver financial solutions through bank systems which they access via APIs which serve as essential components for digital banking in 2026.

Why is cybersecurity important in digital banking?

Cybersecurity protects customer data, which builds trust essential for maintaining future operations of digital banking systems.

How can organisations prepare for digital banking transformation?

Organisations can invest in technology, form partnerships, and provide training on the best digital banking trends that align with recent trends and developments in the banking industry.